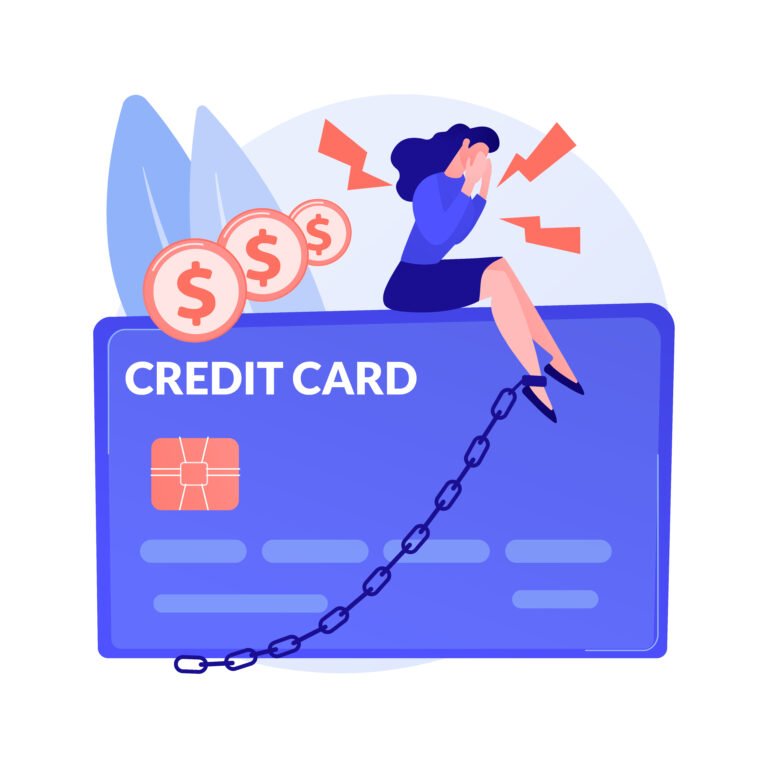

1. When a Merchant Says No: Understanding Your Rights as a Consumer

When a merchant refuses a refund, it can feel like you’ve hit a wall but that doesn’t mean the case is closed. As a consumer, you have rights that allow you to challenge unfair or unfulfilled transactions, and one of the most powerful tools at your disposal is the chargeback process.

First, it’s important to understand why merchants may refuse refunds. Sometimes they rely on strict return policies or hide behind fine print terms. Other times, the merchant may genuinely believe they fulfilled their obligation such as shipping an item that you claim wasn’t received. Unfortunately, there are also cases where businesses operate dishonestly, ignoring complaints or delaying responses in hopes that customers simply give up.

Regardless of the reason, consumers are protected by payment network rules (Visa, Mastercard, Amex) and national consumer protection laws (like the Fair Credit Billing Act in the U.S. or the Consumer Protection Act in India). These frameworks exist to ensure that if you’re wronged whether due to non delivery, defective goods, or billing errors you have a path to resolution.

When the merchant won’t cooperate, your credit or debit card provider can intervene on your behalf through a chargeback. It’s not just a refund request it’s a formal investigation where your bank can reverse the charge and take the funds back from the merchant’s bank.

But timing is key. In most cases, you must initiate the chargeback within 60 to 120 days of the original transaction. You’ll also need proper documentation, like receipts, screenshots, or email correspondence to support your claim.

So if a merchant has refused your refund and you’re left feeling powerless know that you’re not. The chargeback system was created for exactly these situations, and with the right approach, you can recover your money without legal action or endless frustration.

2. What Is a Chargeback and How Does It Work?

A chargeback is a process that allows cardholders to dispute a transaction and request a forced reversal of funds through their bank. Unlike a typical refund (which is handled directly by the merchant), a chargeback goes through your credit card issuer and the payment network. If successful, the funds are returned to your account by reversing the original payment.

Here’s how the process works:

- You file a dispute with your bank or card issuer, stating the reason and providing evidence (e.g., you didn’t receive the item, it was faulty, or the merchant charged you unfairly).

- Your bank investigates the claim and gives you a temporary credit (provisional refund) while they reach out to the merchant’s bank.

- The merchant’s bank reviews the claim and allows the merchant to submit evidence to challenge the chargeback (e.g., delivery tracking, signed receipts).

- Both banks evaluate the evidence and make a decision, often guided by the card network’s rules.

- Final ruling: If your dispute is approved, the temporary credit becomes permanent. If denied, the charge is reapplied to your account.

Card networks use standardized reason codes for disputes, such as:

- Product not received

- Item not as described

- Duplicate transaction

- Unauthorized charge

Importantly, chargebacks are not guaranteed. To improve your odds, your claim must be truthful, well-documented, and aligned with the reason code.

While merchants dislike chargebacks because they involve fees and risk of penalties for too many disputes they serve a vital purpose. They protect consumers from being forced to pay for goods or services that weren’t delivered as promised.

3. Step-by-Step Guide: How to File a Chargeback Effectively

Filing a chargeback is a process that requires attention to detail. Below is a practical, step by step guide to help you navigate the process effectively and improve your chances of getting your money back.

Step 1: Gather Your Evidence

Before initiating the dispute, compile all documentation related to the transaction:

- Order confirmations

- Payment receipts

- Screenshots of product descriptions

- Email or chat conversations with the merchant

- Proof of delivery failure or defect (tracking details, photos)

Step 2: Contact the Merchant (Optional but Wise)

Even if you’ve tried before, one final message requesting a refund (with a deadline) shows good faith and is useful if the bank asks whether you attempted resolution.

Step 3: File the Chargeback With Your Bank

Use your mobile banking app, customer service number, or online portal to start the dispute. Be specific about the issue and match it with the correct dispute reason code.

- Transaction date and amount

- Merchant name

- Why you’re disputing the charge

- Any evidence attachments

Some banks offer online forms, while others may require a phone call.

Step 4: Monitor the Investigation

Once the chargeback is filed, your bank will usually issue a temporary refund while they investigate. You may receive follow-up questions respond quickly and thoroughly.

Step 5: Await the Outcome

If your claim is approved, the chargeback becomes permanent. If denied, you can often appeal with additional evidence or escalate to the financial ombudsman or regulator.

The key to success is clarity, accuracy, and thorough documentation. Chargebacks aren’t about emotion they’re about proving the facts.

4. Real-Life Scenarios: When a Chargeback Can Help

Understanding real-world examples helps clarify when a chargeback is appropriate. Below are several scenarios where a chargeback can protect you and recover lost funds:

1. Non-Delivery of Product

You order a tech gadget from an online store. They send a tracking number, but it shows “pending” for two weeks. After repeated emails, you get no response, and the item never arrives.

Resolution: You file a chargeback under “goods not received,” attach screenshots of the order, shipping issue, and your messages. The bank reviews it and refunds the money.

2. Defective or Misrepresented Product

You buy a “100% cotton shirt” that turns out to be polyester and shrinks after one wash. The merchant refuses a refund, claiming it matches the listing.

Resolution: You provide photos, the product page screenshot, and chat history. The dispute is filed under “item not as described.

3. Cancelled Service Still Charged

You cancel a streaming subscription, receive a confirmation, but are charged again the next month. The company ignores your emails.

Resolution: You file a chargeback for “cancellation not honored,” attach the cancellation proof and billing screenshot, and receive your funds back.

4. Duplicate Billing

You notice you were charged twice for the same hotel booking. The merchant refuses to acknowledge the issue.

Resolution: You file a dispute for “duplicate charge,” show the identical billing entries, and successfully get one reversed.

In each case, the chargeback process acts as a consumer safety net. It ensures you don’t lose money due to errors, fraud, or unresponsive businesses.

5. Avoiding Common Mistakes: Tips for a Successful Chargeback

Filing a chargeback can be straightforward—but many consumers make simple mistakes that reduce their chances of winning. Here are practical tips to avoid pitfalls and strengthen your case.

Don’t Abuse the System

Frequent, unsupported chargebacks can lead to:

- Bank account flags

- Termination of your card

- Legal issues for “friendly fraud”

Only file when the case is legitimate and with solid proof.

Save Everything

Always keep:

- Order confirmations

- Screenshots of listings

- Email/chat transcripts

- Proof of payment and non-delivery

Organized documentation is often what wins a dispute.

Follow Up With Your Bank

Banks may request more details mid-investigation. Check your email and app notifications, and respond promptly. Inactivity can cause the case to close against you.

With the right preparation and mindset, a chargeback is not just possible it’s likely. Follow the rules, stay factual, and you’ll have a strong shot at recovering your funds.

Conclusion: Don’t Let a Refused Refund Be the End of the Story

When a merchant refuses your refund, you have a clear path to justice through the chargeback process. This system is designed to protect you from fraud, billing errors, or dishonest businesses. You don’t have to accept a loss just because a company won’t cooperate.

By understanding your rights, preparing your evidence, and acting within time limits, you give yourself the best chance to win. Thousands of consumers successfully recover their money through chargebacks every day and you can too.

So if you’re stuck after a failed refund attempt, don’t give up. Your bank, your rights, and your voice matter. And when used properly, the chargeback process becomes your most powerful tool to reclaim what’s rightfully yours.